Exotic options: Asian option (FRM T3-46)

my xls is here https://trtl.bz/2Av3F1Y] Asian options are path-dependent: their value depends on the average of the stock price during the life of the option.

Bionic Turtle

Functional Approach to Acceleration of Monte Carlo Simulation for American Option Pricing

We study the feasibility and performance efficiency of expressing a complex financial numerical algorithm with high-level functional parallel constructs.

ACM SIGPLAN

A Quantitative Perspective: The SABR Model & Negative Rates | Numerix Video Blog

http://blog.numerix.com | In this blog Alexandre Antonov discusses global negative rates and the impact on options prices, including the volatility surfaces and ...

numerixanalytics

Black Scholes By Hand Example

This is a video of an example I use in class to introduce the BS OPM to students by hand. After this, we use the spreadsheet as it is much quicker and more ...

Kevin Bracker

Pricing Options via Fourier Inversion & Simulation of Stochastic Volatility Models - Roger Lord

Full workshop available at www.quantshub.com Presenter: Roger Lord: Head of Quantitative Analytics, Cardano Within this workshop we will explore two topics ...

Quants Hub

Valuing an American Option Using Barone-Andesi-Whaley Approximation

We are going to provide an example of valuing American options. We're going to use the Barone-Andesi-Whaley approximation. The Barone-Adesi-Whaley ...

Harbourfront Technologies

Estimating the Implied Volatility of American Options

In this video, I set out a framework for estimating the Implied Volatility of American Call options. I verify my results are consistent with Broadie and Detemple ...

Brian Byrne

Ju Zhong (1999) American Option Pricing

To download C++ code please follow link: https://sites.google.com/view/vinegarhill-financelabs/analytical-american-options Ju Zhong (1999) yields good results ...

Brian Byrne

Ses 12: Options III & Risk and Return I

MIT 15.401 Finance Theory I, Fall 2008 View the complete course: http://ocw.mit.edu/15-401F08 Instructor: Andrew Lo License: Creative Commons BY-NC-SA ...

MIT OpenCourseWare

Steve Heston -- Recovering the Variance Premium

Steve Heston (University of Maryland) presents his new paper titled "Recovering the Variance Premium." The slides and the paper are available at ...

Virtual Derivatives

Stefano De Marco: Some asymptotic results about American options and volativity

Abstract: The valuation of American options (a widespread type of financial contract) requires the numerical solution of an optimal stopping problem. Numerical ...

Centre International de Rencontres Mathématiques

Leisen Reimer up close 2

In this video I look at the Leisen Reimer binomial option pricing model. I consider three versions of the model set up in C++. (1) Static (2) Dynamic (3) Dynamic ...

Brian Byrne

10. How to Price Options Based on Implied and Historical Volatility

Try a free options trading demo account here: http://bit.ly/Q72dYG For more of our free introductory options course, go here: http://www.informedtrades.com/f115/ ...

InformedTrades

Binomial model

paulmullan.

Colin Ohare

Is the Black Scholes Actually Used in the Real World

A subscriber asked if the Black-Scholes model you learn is school is used in the real world. And also if the theory is actually applicable. The short answer is yes, ...

Dimitri Bianco

Option Valuation - Binomial Model

Learning Objectives Know what is binomial model Understand the steps to calculate premium of call option Understand the steps to calculate premium of put ...

S. B. J. S. Rampuria Jain College, Bikaner

Neural Networks for Hedging Strategies in a Mean-Variance Incomplete Markets Framework.

In this video, we talk to Yuri Robbertze who is a maths student at the University of Cape Town. You can access his paper on his LinkedIn profile page: ...

MJ the Fellow Actuary

American vs European Futures Options 1

Please find Leisen Reimer VBA code below: ...

Brian Byrne

Valuing an American Option Using Binomial Tree-Derivative Pricing in Excel

We're going to use the binomial pricing model to value an American equity option. Essentially, the model uses a “discrete-time” model of the varying price over ...

Harbourfront Technologies

The Leisen Reimer Binomial Tree implemented using C++ code Part 1

To retrieve Leisen Reimer C++ code: https://1drv.ms/w/s!AsWcG8zbg1hc5jd6WNuchlpiM1jj To retrieve Leisen Reimer code for Implied Volatility: ...

Brian Byrne

Simon Byrne: Composable financial contracts with Miletus

Julia Computing

Calculating Implied Volatility from an Option Price Using Python

I look at using Newton's method to solve for the implied volatility of an option. This is done using the Black-Scholes model and a simple Python script. My mouth ...

Kevin Mooney

Sparse Gaussian Process Approximations, Richard Turner

Sparse Gaussian Process Approximations Richard Turner University of Cambridge http://gpss.cc/gpss17/slides/gp-approx-new.pdf Wednesday 11am For the full ...

Michael Smith

Episode 7 - Steiner Trees

This episode will cover Steiner Trees and techniques for efficient solutions for different constraints. 00:00 - Welcome 01:40 - Introduction to Steiner Trees 03:50 ...

Algorithms Live!

Webinar: Better Approaches to American Style Options Pricing

Director of Quantitative Analysis, David Hrencecin discusses the Whaley and Ju-Zhong models, which are both analytic approximation methods for getting ...

Vela

Python Code for Cox Ross and Rubinstein evaluating American Options

To retrieve code, please follow link to: https://sites.google.com/view/vinegarhill-financelabs/binomial-lattice-framework/cox-ross-and-rubinstein.

Brian Byrne

No-arbitrage pricing 02 - Option pricing

Course website: https://sites.google.com/view/aaaacademy/money-and-banking Pre-requisites No-arbitrage pricing 03 - Fruit basket example.

A&A Academy

Adaptive Sampling via Sequential Decision Making - András György

The workshop aims at bringing together researchers working on the theoretical foundations of learning, with an emphasis on methods at the intersection of ...

The Alan Turing Institute

Alexandre Zhou -- Existence to a calibrated regime-switching local volatility model

http://www.lesprobabilitesdedemain.fr Organisateurs : Linxiao Chen, Benoît Laslier, Pascal Maillard, Bastien Mallein, Sébastien Martineau, Damien Simon et la ...

Probabilités de Demain

Webinar - Time Critical American Option Pricing

Hosted by: David Hrencecin, Head of Quantitative Analysis Iqbal Brainch, VP of Product and Marketing Strategy OptionsCity has several pricing models that are ...

Vela

Research in Options 2016 - Yuri Saporito | Uwe Schmock | Rodrigo Targino

Research in Options 2016 Risk & Derivatives (part III) Yuri Saporito (FGV, Brazil) Uwe Schmock (TU Vienna) Rodrigo Targino (FGV, Brazil) Página do Programa: ...

Instituto de Matemática Pura e Aplicada

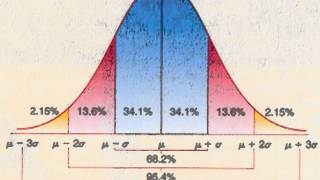

Market maker's delta-hedge illustrated (FRM T4-20)

my xls is here https://trtl.bz/2O1OwKT] This market maker writes one call option (to the client) and hedges delta by purchasing Δ shares of the stock; this ...

Bionic Turtle

Maplesoft solutions for advanced financial modelling

For more information, visit us at: http://www.maplesoft.com/products/MapleSim/?ref=youtube.

Maplesoft

FRM Part 2 : Hazard Rate / Default Intensity and it's Interpretations

In this short video from FRM Part 2 (Credit Risk section), we explore the various interpretations of the hazard rate / default intensity - a construct that we ...

finRGB

Professor Emanuel Derman: Models Behaving Badly

Emanuel Derman talks about his experiences in both the financial and physics world while exploring the collision between human needs and desires, ...

Institute of Physics

21. Stochastic Differential Equations

MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: http://ocw.mit.edu/18-S096F13 Instructor: Choongbum ...

MIT OpenCourseWare

Kristoffer Andersson (CWI), Learning exposure profiles for portfolios of exotic derivatives

Kristoffer Andersson is a PhD candidate in the group of Prof. Kees Oosterlee. He is currently working, in the context of a European Industrial Doctorates project, ...

CentrumWI

Research in Options 2017 - Uwe Schmock (Vienna University of Technology)

Research in Options 2017 - Uwe Schmock (Vienna University of Technology) IMPA, Rio de Janeiro, November 25 – 30, 2017 Uwe Schmock (Vienna University ...

Instituto de Matemática Pura e Aplicada

Introduction to Black-Scholes

In this advanced lesson we will look at the Black-Scholes model and how it can help us understand how options are priced. Options had been around for many ...

Options In Plain English

Advanced Derivatives: Geometric Brownian Motion and Option Trading..

tastytrade explains how the Black-Scholes model assumes that underlyings move according to a geometric brownian motion. Other option pricing approaches ...

tastytrade

NeurIPS 2019 | Deep Learning with Bayesian Principles by Mohammad Emtiyaz Khan

Continue to support the channel: https://paypal.me/aipursuit https://slideslive.com/t/neurips-2019 for more videos with slides. As this is a non profit channel, ...

AI Pursuit - Advancing AI Research

COMPLETE AQA A-Level Maths Specimen Material Paper 2

Find all the papers here: http://bit.ly/TLMathsPapers Find easy navigation to the videos for this playlist here: ...

TLMaths